Most people assume their insurance covers generic drugs cheaply. But here’s the truth: bulk buying and tendering is what actually drives those low prices-and most policyholders never see the full picture. Insurers don’t just pay what pharmacies charge. They use complex bidding systems, volume contracts, and formulary rules to cut costs by up to 90%. This isn’t magic. It’s procurement strategy-and it’s saving billions every year.

How Generic Drugs Became the Key to Cost Control

In 1984, the Hatch-Waxman Act changed everything. It made it easier for companies to make copies of brand-name drugs after patents expired. Suddenly, there were dozens of manufacturers competing for the same pill. That competition is what made generics possible. Today, 90% of all prescriptions in the U.S. are for generics. But they only make up 17% of total drug spending. That gap? That’s where the savings live.

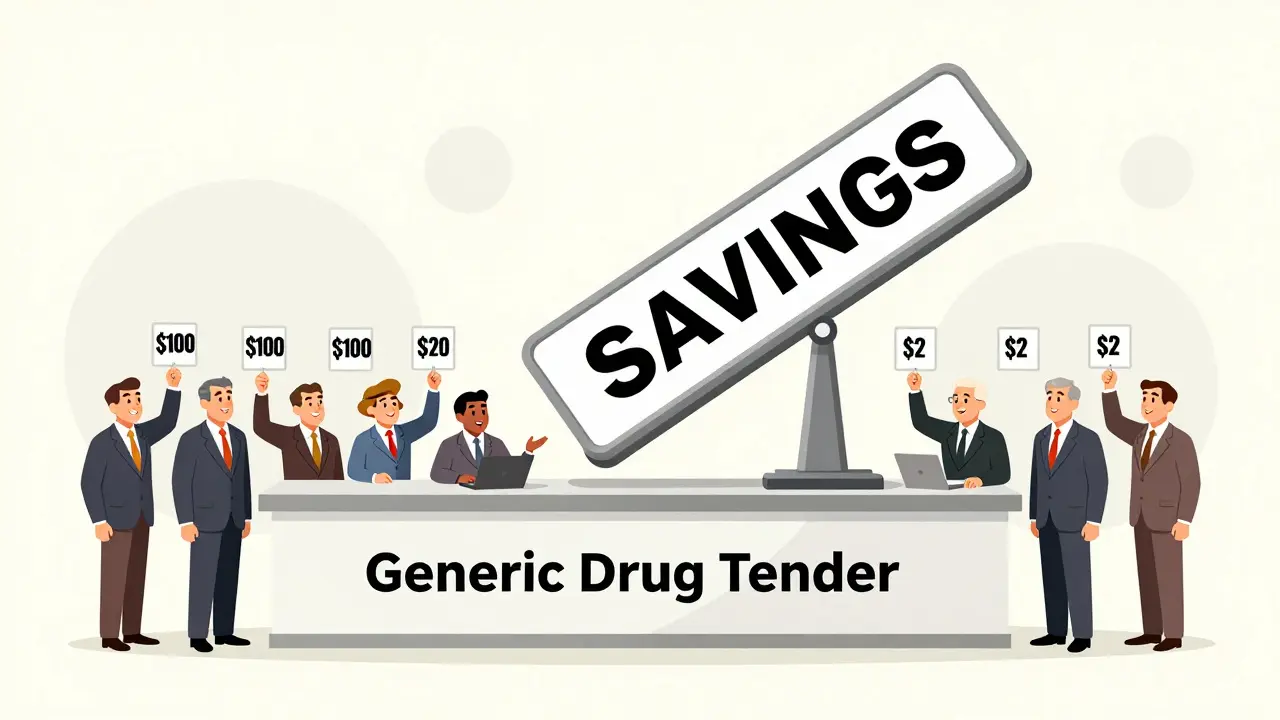

Insurers don’t just accept whatever price a pharmacy offers. They run tendering processes-essentially auctions-for high-volume generic drugs. For example, if a drug like metformin (used for diabetes) has 15 different manufacturers, the insurer invites them all to bid. The lowest bidder wins the contract. But here’s the catch: the insurer guarantees they’ll buy millions of pills over the next year. That volume gives manufacturers the confidence to slash prices.

The Hidden System: MAC Lists and Tiered Formularies

Behind the scenes, insurers use something called Maximum Allowable Cost (MAC) lists. These are secret price caps for generic drugs. If a pharmacy tries to charge more than the MAC, the insurer pays only the capped amount-and the pharmacy eats the difference. Many independent pharmacies hate this. A 2023 survey found 42% said their margins on generics had shrunk so much they were barely breaking even.

Insurers also use tiered formularies. Generics usually sit on Tier 1, with $0-$10 copays. Brand-name drugs? Tier 3 or 4, with $25-$60. But here’s the twist: a 2024 report from the Association for Accessible Medicines found that 78% of Medicare Part D plans still put generics on higher tiers than they should. Why? Because some pharmacy benefit managers (PBMs) make more money when patients pay more-even for generics.

Spread Pricing: The Industry’s Dirty Secret

Most people don’t realize that PBMs (like OptumRx, Caremark, and Express Scripts) aren’t just middlemen. They’re profit centers. In spread pricing, the PBM tells the insurer, "We negotiated a $10 price for this generic." Then they pay the pharmacy $6. They pocket the $4 difference. The insurer thinks they’re saving money. The patient pays the same copay. But the PBM gets richer.

A 2022 JAMA Network Open study showed this practice is widespread. Plan sponsors-like employers or health plans-often don’t even know how much the PBM is keeping. That’s why states like California passed laws like SB 17 in 2017, forcing PBMs to disclose any price differences over 5%. Transparency is the only way to fix this.

When the System Breaks: Generic Shortages

There’s a dark side to extreme price pressure. When insurers push prices too low, manufacturers can’t make a profit. In 2020, albuterol inhalers-the go-to rescue inhaler for asthma-disappeared from shelves. Why? The price had dropped below the cost of production. A 2021 survey by the American Society of Health-System Pharmacists found 87% of hospitals reported shortages.

This isn’t an accident. It’s a consequence of tendering without limits. The FDA has warned that too few manufacturers now make most generics. In some drug classes, just three companies produce 80% of the supply. That’s not competition. That’s a monopoly waiting to happen.

What Works Better: Transparent Pricing Models

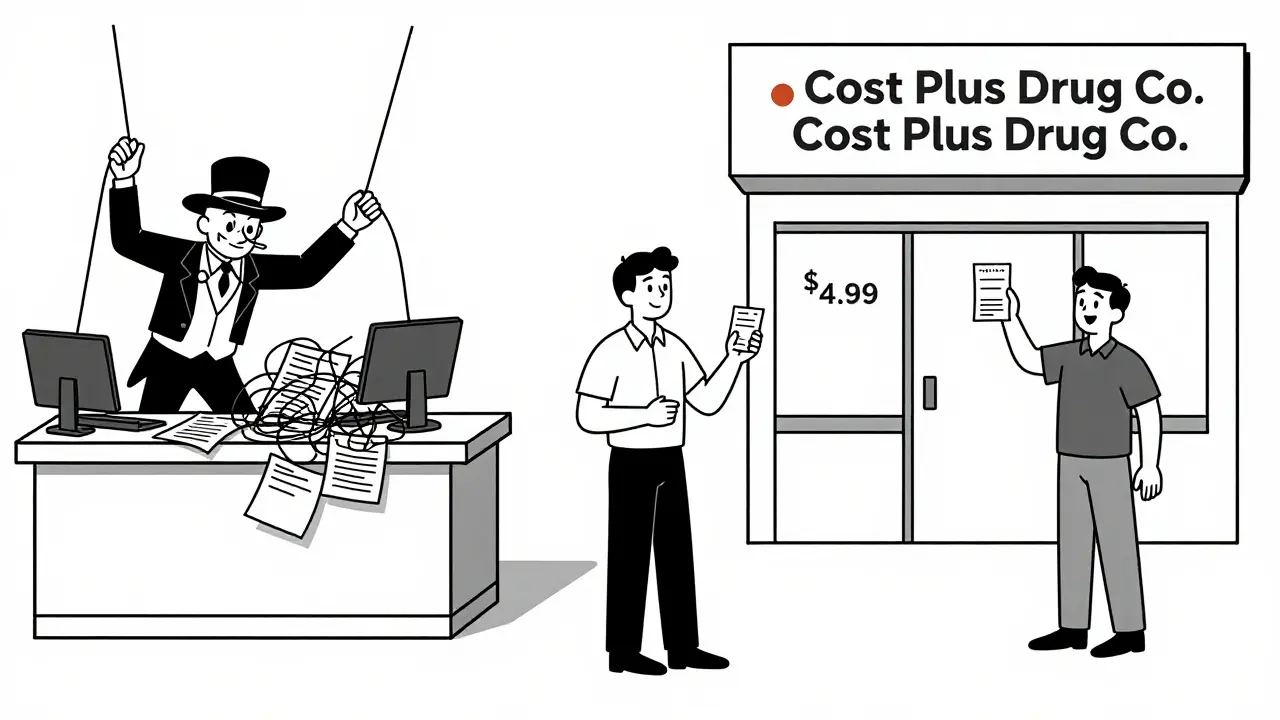

There’s a growing movement to cut out the middleman entirely. Companies like Mark Cuban’s Cost Plus Drug Company and GoodRx don’t negotiate with PBMs. They buy directly from manufacturers and sell at cost plus a fixed fee-usually 15%. The result? Patients pay 75-91% less than retail.

One Reddit user paid $87 for a generic prescription through insurance. The same drug at Cost Plus Drug Company? $4.99. A GoodRx user reported saving $32 a month on three generics by ignoring insurance altogether. In 2020, 97% of cash payments for prescriptions were for generics-because people realized insurance wasn’t helping.

Blueberry Pharmacy, which uses transparent pricing, has a 4.7/5 rating on Trustpilot. One customer wrote: "My blood pressure med costs exactly $15/month. No surprises. No insurance drama." That’s the kind of predictability insurers could offer-if they chose to.

How Insurers Can Do Better

Effective tendering isn’t about lowest price. It’s about smart price. Here’s what works:

- Review your formulary every quarter. Look for generics with fewer manufacturers-they’re less competitive and more expensive.

- Require PBM contracts to disclose spread pricing. California’s law proves it’s possible.

- Partner with transparent pharmacies. Offer members a $0 copay option at Cost Plus Drug Company or similar.

- Use first generics aggressively. The FDA found the first generic version of a drug saves over $1 billion in its first year.

- Don’t assume all generics are equal. Some are made in the same factory as the brand-name version-others aren’t. Quality matters.

A 2023 study by Navitus Health Solutions found their employer clients saved 22% on generics compared to traditional PBM models. That’s not a small win. That’s millions in savings.

The Bigger Picture: Why This Matters

In 2023, generics saved the U.S. healthcare system $445 billion. $194 billion of that went to people aged 40-64-the group most likely to need chronic meds. But savings aren’t automatic. They’re fought for. They’re negotiated. They’re won by insurers who stop treating pharmacy benefits like a black box.

Right now, Medicare Part D pays 80% less than it did in 2007. The Veterans Health Administration pays 24% less than Medicare. Why? Because they negotiate directly. No PBMs. No spreads. No secrets.

Insurers that cling to opaque, profit-driven models aren’t just overpaying. They’re forcing patients to choose between meds and rent. A KFF survey found 68% of Medicare beneficiaries have thought about skipping a dose to make a prescription last. 41% actually did it.

This isn’t just about cost. It’s about trust. And trust is broken when patients pay more for generics than they would if they paid cash.

What’s Next?

The Inflation Reduction Act of 2022 didn’t fix the PBM problem. It left the incentives for high-priced generics intact. But change is coming. The FDA’s GDUFA III program, launched in 2023, is speeding up generic approvals. CMS now requires Medicare Part D plans to disclose pricing details. And new PBM alternatives like Navitus are proving you don’t need a 30-year-old system to save money.

The future belongs to insurers who treat drug pricing like a supply chain problem-not a profit center. Those who do will save money. Those who don’t will keep losing patients to cash payments and direct-to-consumer pharmacies.

Why are generic drugs so much cheaper than brand-name drugs?

Generic drugs are cheaper because they don’t need to pay for research, clinical trials, or marketing. Once a brand-name drug’s patent expires, other companies can make identical versions. The competition drives prices down-often by 80-90%. The first generic version of a drug can save over $1 billion in its first year.

Do insurers really save money with bulk buying?

Yes. Bulk buying lets insurers negotiate lower prices by promising to buy large volumes over time. For example, if an insurer commits to buying 10 million pills of a generic blood pressure drug, manufacturers will offer a much lower price per pill than if they sold one at a time. This is how insurers save billions annually.

What is spread pricing and why is it a problem?

Spread pricing is when a pharmacy benefit manager (PBM) charges an insurer one price for a drug, pays the pharmacy a lower price, and keeps the difference. The patient pays the same copay, but the PBM pockets the profit. This hides the true cost of drugs and gives PBMs an incentive to choose more expensive generics-even when cheaper ones exist.

Can I save money by paying cash for generics instead of using insurance?

Absolutely. Many cash prices at pharmacies like Cost Plus Drug Company, Walmart, or GoodRx are lower than insurance copays-even with a discount. A 2023 NIH study found cash prices for expensive generics were 76% lower than retail. If your insurance copay is over $15, it’s worth checking cash prices first.

Why do some generic drugs have shortages?

When insurers and PBMs push prices too low, manufacturers can’t make a profit. If a drug costs $2 to make but the market price is $1.50, companies stop making it. That’s what happened with albuterol inhalers in 2020. Only a few companies make most generics, so when one stops production, shortages follow.

What’s the difference between a PBM and an insurer?

An insurer (like Blue Cross or Aetna) pays for your health care. A PBM (like CVS Caremark or OptumRx) manages your drug benefits-they negotiate prices with pharmacies and set formularies. Many PBMs are owned by insurers, creating a conflict of interest. They profit from high prices, even if it hurts patients.

Are all generic drugs the same quality?

Legally, yes-they must meet FDA standards. But in practice, some are made in better facilities than others. The same factory often makes both the brand-name and generic version. If your drug isn’t working right, switching to a different generic manufacturer can help. Ask your pharmacist which company makes your pill.

What You Can Do Today

If you’re a patient: Always check cash prices. Use GoodRx or Cost Plus Drug Company. Compare them to your insurance copay. You might be paying more than you need to.

If you’re an employer or plan sponsor: Demand transparency from your PBM. Ask for the spread pricing numbers. Switch to a model that pays a flat fee instead of taking a cut.

If you’re an insurer: Stop treating generics like a mystery box. Run real tendering. Reward manufacturers who deliver quality at low cost. And stop letting PBMs profit from your members’ health.

The system isn’t broken. It’s working-for someone. It’s time it worked for you.

Jake Kelly

Really eye-opening breakdown. I had no idea PBMs were pocketing the difference like that. Crazy how patients are stuck paying the same copay while the middlemen get richer.

lisa Bajram

OMG I just checked my blood pressure med-$48 with insurance, $12 cash on GoodRx. I’ve been throwing money away for years. Why does no one tell you this?!?!

Ashlee Montgomery

The real tragedy isn’t the spread pricing-it’s that people are skipping doses because they can’t afford the copay even when the drug costs pennies to produce. We’ve turned healthcare into a casino where the house always wins. And the worst part? Most patients don’t even know the rules.

Paul Bear

Let’s be precise: PBMs are not intermediaries-they’re rent-seekers. Their business model is predicated on information asymmetry, regulatory arbitrage, and the systemic inability of plan sponsors to audit their contracts. The structural failure here is not incidental-it’s intentional, and it’s enabled by the lack of fiduciary duty imposed on them under ERISA.

neeraj maor

Of course the system’s rigged. Big Pharma owns the FDA, the PBMs own the insurers, and Congress owns them all. You think this is about savings? It’s about control. The same people who make you pay $100 for insulin also run the algorithms that decide which generics get approved. They want you dependent. They want you scared. They want you paying.

Michael Marchio

Look, I get it-bulk buying saves money. But you can’t just squeeze manufacturers until they stop making drugs. It’s like cutting wages to save on payroll and then wondering why no one shows up to work. The FDA’s own data shows that for 120+ generic drugs, there are only one or two manufacturers left. That’s not competition-it’s a hostage situation. And now we’re paying the price with shortages of epinephrine, antibiotics, even thyroid meds. You want low prices? Fine. But you also need a supply chain that doesn’t collapse when one plant has a power outage. That’s not rocket science. It’s basic risk management. And no one’s doing it.

Then you’ve got these ‘transparent’ pharmacies like Cost Plus Drug Company. Great. But they’re niche. They don’t cover everything. And they’re not integrated with insurance networks. So now you’ve got a two-tier system: the wealthy who can afford to opt out, and the rest of us stuck in the broken system. That’s not progress. That’s segregation with a better UI.

And let’s not pretend the answer is just ‘pay cash.’ What about people on fixed incomes? What about seniors on Medicare who don’t have the time or tech savvy to compare prices across five different apps? What about rural folks who don’t have a Cost Plus pharmacy within 50 miles? This isn’t a consumer choice problem. It’s a structural policy failure. And until we treat drug pricing like a public good-not a profit center-we’re just rearranging deck chairs on the Titanic.

Navitus saved 22%? Cool. But how many employers even know what Navitus is? How many people know their PBM’s name? How many patients realize their ‘copay’ isn’t even going to the pharmacy? We’re not just overpaying-we’re paying blindfolded. And the worst part? The people who designed this system are still getting bonuses.

Kunal Majumder

Bro, I used to pay $60 for my metformin. Now I get it for $3 at Walmart. No insurance needed. Just walk in, ask for the cash price. Life changed.

Aurora Memo

It’s heartbreaking to see how many people are forced to ration their meds. I’ve had patients cry telling me they skipped doses because they couldn’t afford the copay-even though the drug cost less than a cup of coffee to make. We need to stop pretending this is about ‘efficiency.’ It’s about dignity.

Ted Conerly

Love the actionable steps at the end. Especially #4-first generics are the golden ticket. I’ve seen employers cut their generic spend by 30% just by switching to the first approved version every time. Simple. Effective. No drama.

Jaqueline santos bau

Wait… so you’re telling me my insurance is literally stealing from me and I’m the one getting blamed for high premiums?!?! I’m so done. I’m switching to cash. And I’m telling everyone I know. This is a scam.

Ritwik Bose

Thank you for this detailed analysis. 🙏 It is truly important to recognize that systemic reform is required-not merely individual workarounds. The dignity of human health must not be commodified. Let us hope that transparency becomes the new standard.

chandra tan

India makes 40% of the world’s generics. But here’s the twist-most of the good stuff is exported. The cheap ones we get here? Made in factories with bad air quality and no OSHA. You think you’re saving money? You’re just importing risk.

Dwayne Dickson

Let me be clear: the PBM model is not a business innovation. It is a regulatory capture play. The fact that 97% of cash payments for prescriptions are for generics? That’s not a market signal. That’s a referendum. And the market voted ‘NO’ to the current system.

Faith Edwards

It is profoundly disturbing that a nation capable of landing rovers on Mars cannot ensure its citizens access basic, life-sustaining medications at a fair price. The moral bankruptcy of this system is not merely a policy failure-it is a civilizational one.